Health Insurance for Long-Term Nomads in Asia

Let's get real for a second. You're sipping a coconut on a Thai beach, living the dream. But that dream can turn into a financial nightmare quicker than you can say "food poisoning." Hospitals in Asia are no joke. They're modern, efficient, and they will absolutely expect payment upfront. That motorbike scrape? That weird fever? Without a plan, you're one x-ray away from wiping out your savings. Travel insurance for a two-week vacation ain't gonna cut it here. You need something built for the long haul.

Asia's Healthcare Game: A Mixed Bag

Here's the thing about Asia: the healthcare quality is a wild rollercoaster. You've got world-class facilities in Bangkok and Singapore that rival the West. And then you've got rural areas where the best option might be a bumpy scooter ride to a clinic. Your insurance needs to cover both extremes. A cheap local policy might only work in one country. That's useless when you're bouncing from Bali to Vietnam to Japan. You need coverage that doesn't care about borders, because your laptop lifestyle certainly doesn't.

What Actually Matters in a Nomad Plan

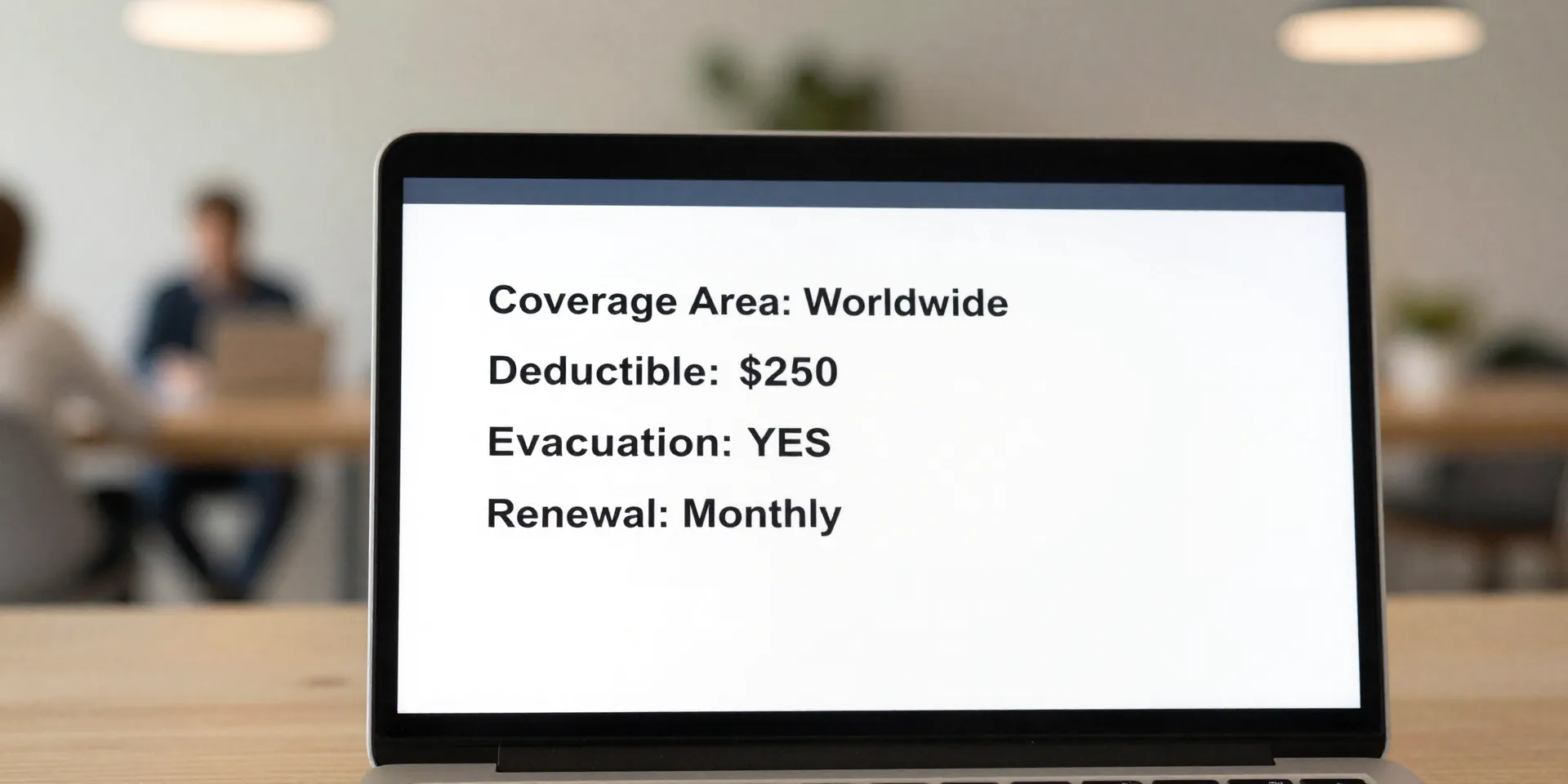

Forget the slick sales jargon. You need to look for three brutal realities. First: true geographic flexibility. Global coverage, or at least a massive region. Second: a sensible deductible. The $50 ones are a trap—your premium will be insane. Aim for $250-$500; it keeps costs down for the small stuff you can handle. Third, and most critical: medical evacuation. If something really bad happens in the islands, they need to fly you to a proper hospital. If your plan doesn't have "medevac," close the tab. It's that important.

SafetyWing: The Nomad-Favorite, Unvarnished

Alright, let's talk about the elephant in the co-working space. Yes, SafetyWing is huge with remote workers. And for good reason. It's designed for us: subscription billing, covers you while you're briefly back home, and it's relatively painless to sign up. But it's not perfect. It's bare-bones. Customer service can be slow. For serious, chronic conditions, you might want something beefier. Think of it as the reliable, affordable base layer. It gets the job done for most people, most of the time. That's its strength.

Don't Just Check the Box, Read the Fine Print

This is where people mess up. They buy the plan and feel relief. Actually, the real work starts now. You have to *understand* your policy. What's the claims process? Do you pay upfront and get reimbursed (common)? What's excluded? Spoiler: pretty much every plan excludes "high-risk activities." That might mean motorbiking in Vietnam. Be honest about your lifestyle. The worst time to discover an exclusion is in an emergency room. A few boring hours reading now saves a world of pain later.